I’m going to be completely honest with you—some insurance companies have lost their damn minds with these premiums.

Just last week, I talked to someone paying over $300 a month for liability only. LIABILITY. That’s insanity.

Being in the industry, I see this kind of thing every day. Sometimes I can help folks save a ton—other times, even my carriers are way out of line. But here are some solid tips to help you save money on your policy. I’d bet money you’ve never heard the last one.

#1: Shop Around Seems obvious, but most people don’t do it. We’re creatures of habit—and let’s be real, nobody enjoys shopping for insurance. I stayed with Geico for nine years without checking. Big mistake. I was overpaying the entire time.

#2: Pay in Full If you can swing it, paying your auto premium in full can save you 10–15% or more. That could mean hundreds of dollars in savings. Not a bad payoff for skipping the monthly billing cycle.

#3: Ask for a Re-Quote After Major Life Changes Life happens—and when it does, your rate can change. But only if you tell your insurance company. Things like marriage, retirement, switching to a remote job, buying a home, or improving your credit score can all lower your premium. Ask for a re-quote and see what happens.

#4: Bundle Your Policies Still underrated. Bundling your home or renter’s insurance with your auto can knock up to 25% off your car premium and around 10% off your home. If you haven’t looked into this, you might literally be throwing money away.

#5: Dispute Bad Info on Your Record Here’s a good one: I recently helped a guy who was trying to add his daughter to his policy, but thanks to a mystery claim on her driving record, he was about to get charged out the ass. Turns out the claim “happened” before she was even born. We called LexisNexis (the company that reports accident and ticket data to insurance carriers), disputed it, and poof—solid rate unlocked. If something doesn’t look right, call LexisNexis at 1-800-543-6862 and dispute it. You might be surprised what’s on your report.

Anything I missed? Any tips and tricks that you have? Drop them below in the comments.

When it comes to leads, there’s a whole lot of conversation on Reddit and other online Insurance Forums about what sources of leads are working for people. Is it referrals? Is it online leads? Live call transfers? Really, I think depending on your line of business, your current situation as an agent, and whether you’re captive or independent can all play a role in what makes the most sense for you. Obviously, I’d rather just have people lining up outside my office taking numbers and waiting for me to scream, “NEXT!”

Maybe in another life. I’d rather not have to buy leads, but the fact remains that for most new agents, leads are the best way to consistently have conversations with potential clients. In my line of business, it’s pretty much a numbers game. Ten conversations a day almost always guarantees at least one sale. Sometimes more.

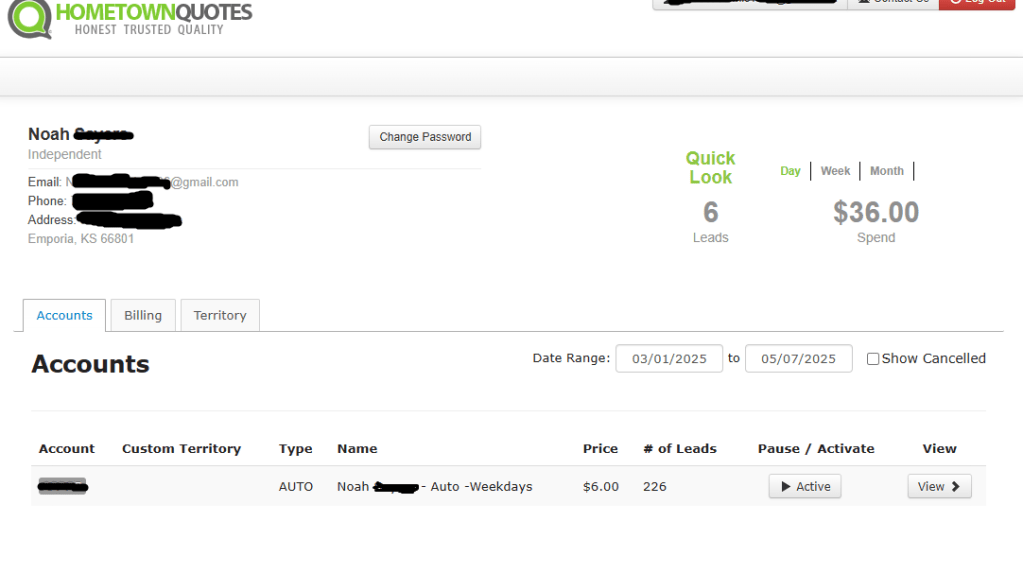

For the past couple of months, I’ve been using Hometown Quotes—and Joe, if you’re reading this, thanks for getting in touch with me and getting me linked up with a killer lead vendor.

Look—I’m not going to say that the leads are perfect because they’re not. No source of leads is. However, for all intents and purposes, I think Hometown Quotes does a pretty solid job of providing affordable leads that are still high-intent and worthwhile.

226 leads in two months… yeah, I’ve got a problem.

Let’s talk about the good, the bad, and the fugly about Hometown Quotes. Overall? Yes, I like the service. Hopefully, if someone from Hometown Quotes is reading this, they can get to “the powers that be” about the bad and the fugly.

The good:

At six bucks a lead, there are basically no other lead services that even compare—at least as far as I know. If you know of something cheaper, drop a link in the comments and I’ll check them out

These leads are genuinely high intent—they’re folks who actually want quotes and are ready to talk

Highly customizable filters that let you target exactly the kind of leads you want

Unlimited returns on most leads, especially for disconnected numbers

TCPA compliant with full documentation—timestamps, IP addresses, and proof of consent included

The bad:

You’ll get your share of cheapskate clients looking for bare-minimum coverage. Not ideal if you prefer selling better coverage, though filters can help

Expect some disconnected or wrong numbers. It happens, but you can return these and move on

These are shoppers—be prepared for occasional chargebacks unless you build a solid relationship with the client

The fugly:

Unfortunately, I’ve found that about 5% or so of these leads will try their best to make your life hell – literally! They’ll scream and curse you out as soon as you dial their number or send them a text. I don’t take it personally, and I just return those leads.

Conclusion:

If you can afford to drop $6 for a chance to make a sale and get folks on the books, Hometown Quotes is a solid option for independent agents and captives alike. Like with all lead vendors, there are pros and cons. Personally, my average cost per policy is about $30–$40. Generally speaking, I stand to 4x or 5x my investment. Your mileage may vary depending on which carriers you have access to AND your own personal sales process. Personally, Hometown Quotes blows other services such as Aged Leads Store out of the water.

I’m still very much a greenhorn in insurance sales, so take my advice with a grain of salt. I spend a lot of time on Reddit and other online platforms, checking out what other agents are doing—whether they’re buying certain types of leads or sharing tips on how to get ahead. A conversation that comes up a lot is whether you should sell as an independent broker or as a captive agent. I’ve done both, and here are my unfiltered thoughts.

When I worked as a captive agent at Allstate, I learned that having a strong brand behind you really helps. Just saying “This is Noah with Allstate” instantly gives you credibility over a less-known name. That familiar ring makes it easier to get people to agree to a quote in those critical first few seconds of the call. However, there’s a downside. Captive agents only have one product per insurance line. So, if you need to lower a rate, your options are limited—you’re confined to suggesting things like enrolling clients in driving-monitoring programs or reducing coverage. Both paths invite objections and place you in a pushy, high-pressure sales role.

In contrast, being an independent broker gives you a buffet of options. You don’t have strict quotas, and you’re free to act more like a trusted advisor than a hard sell. Sure, a captive agency’s brand and training can be great—especially for your first six months to a year—but independent work lets you tailor your approach, offer multiple solutions, and save customers money without feeling like you’re forcing a sale.

Captive Pros

Captive Cons

Independent Pros

Independent Cons

Brand recognition

Less options

More options

Less brand recognition

Simpler to work with

Corporate kool-aid sessions

Can focus more on the client’s needs than making the sale

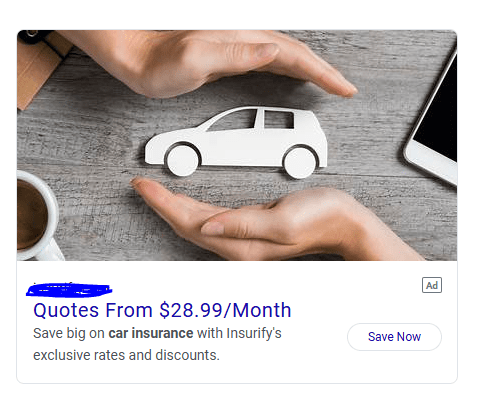

Have you ever scrolled through Facebook and come across an ad that seemed too good to be true? Of course, you have. Unfortunately, social media platforms like Facebook rarely vet the ads they host. This issue extends to the internet as a whole.

In just ten minutes of scrolling, you’re likely to see a couple dozen ads, some of which might look something like this:

The image above is an example of a misleading ad you might encounter. It’s tempting to click and see your options, but once you submit your information, it’s likely to be sold. By filling out the form, you’ve agreed to this—and soon, a dozen insurance agents might be calling. If you’re okay with that and willing to sift through the calls, you might find a better deal. However, $28.99 a month for even just liability is nearly unheard of in my industry, especially in Kansas. Ads like this set a dishonest expectation for customers.

While these ads seem convenient, they often do more harm than good. If you’re shopping, go to a local agent or broker instead. You’ll get a better experience by working with someone who knows your needs and will be there for you when it counts.

Any questions? I “Noah” guy. Comment below or reach out to me via email: Noah@Theelinsurance.com

Ahh, Emporia! If you love disc golf, great food, and good vibes, this is the place to be—and it’s my home. Since moving here in 2019, I’ve fallen in love with Emporia’s tight-knit community. Because I live here, and many of the people I serve do too, I thought it was only fitting to create a Rate Guide for Emporia, just like I did for Wichita.

The graph below is a great starting point if you’re shopping for car insurance and aren’t sure which company offers the best rate. Of course, your personal situation will affect your monthly premium, but these numbers give you a rough idea of what the average driver in Emporia might pay. The blue bar shows liability-only coverage at state minimums, while the pink bar represents full coverage with higher liability limits.

Rates can vary a lot depending on your situation—there’s no one-size-fits-all insurance company. Personally (and yes, I’m a bit biased), I recommend letting a broker shop around for you.

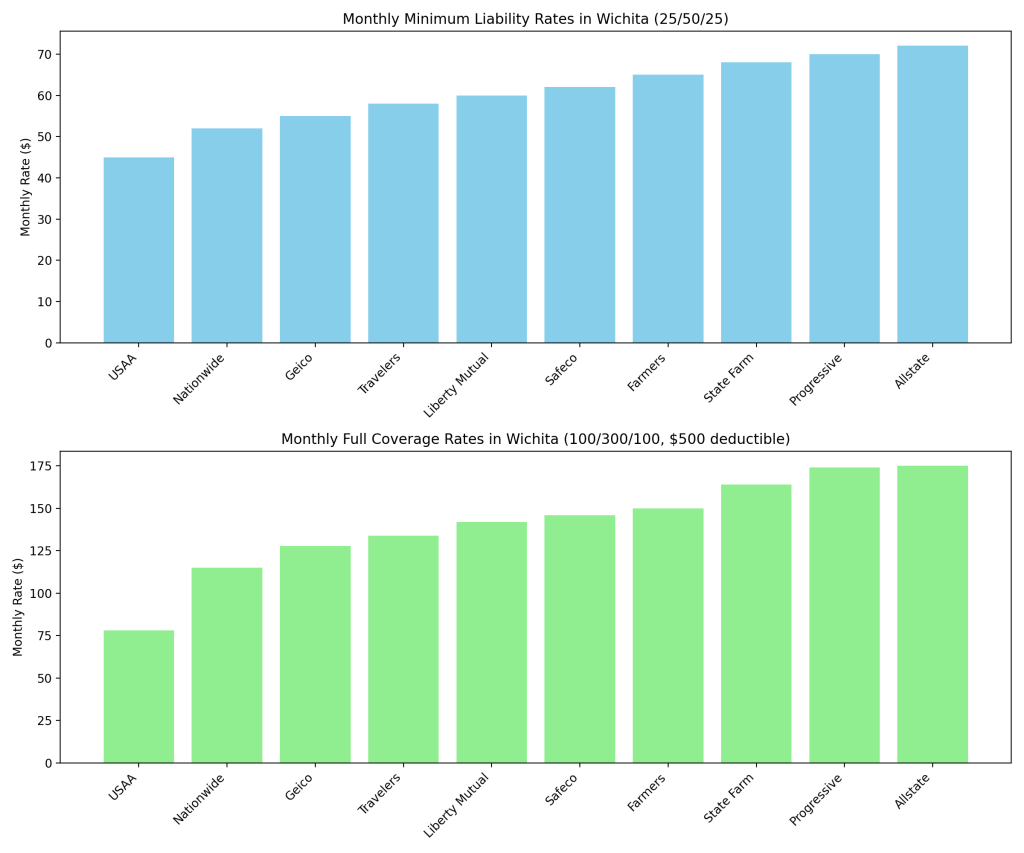

Wichita is the most populous city in Kansas, which means there are plenty of risks that come with living and driving here every day.

One major challenge when shopping for insurance in Wichita is simply the number of other drivers on the road. It might sound obvious, but more drivers can mean higher car insurance rates—and a bigger hit to your wallet. Other factors, like crime rates and annual accidents in your ZIP code, also play a role.

All of this can make shopping for car insurance feel overwhelming, especially if you’re collecting quotes from individual carriers one by one. That’s why I’ve put together a couple of graphs to give you a sense of what the top 10 carriers in the area might charge. Of course, these aren’t guarantees—you’ll need to get quotes directly from the carriers to know your exact rate.

As you’ll see, premiums can vary widely depending on the company. Generally, USAA is the cheapest if you’re military-affiliated, while Allstate tends to be on the higher end.

Personally, I recommend using an insurance broker to shop around for you. But if you’re set on comparing companies yourself, this is a great place to start.

Looking for information about which carriers might fit your needs more specifically? Check out my article: Choosing the Right Car Insurance.

Any questions? I “Noah” guy. Comment below or reach out to me via email: Noah@Theelinsurance.com

Car insurance can be a tricky subject. Coverages are often confusing, and each carrier calculates your monthly premium differently. To make matters worse, many agents don’t take the time to explain what you’re actually buying. That makes it hard to figure out which options are the best fit for you.

Most people end up shopping based on price — and that can take forever, especially if you’re looking for specific coverages. It’s important to understand how your unique situation impacts your premium, which is why rates can vary so much from one company to the next. A friend once told me that car insurance is “like a casino,” and honestly, I couldn’t agree more.

When shopping for car insurance, there are some things you should consider:

Recent accidents, tickets, or claims on your record

How long your current policy has been in effect

The coverages you need

Your age

Make and model of your vehicle(s)

Bundling discounts from things like home and renters insurance.

I usually recommend working with a broker. They can shop multiple companies at once and offer a wider range of options — plus, it’s often quicker and easier than going company by company.

If a broker’s not your thing, no worries. Below, I’ve included a table of carriers to help you compare on your own.

Younger Drivers (16-25)

Geico, State Farm, USAA (if military affiliated)

Older Drivers (55+)

Allstate, State Farm, The Hartford

Low Mileage and Work From Home Drivers

Allstate, Nationwide (Both have pay-per-mile plans)

Families with Teen Drivers

Progressive, State Farm, Allstate

Drivers with Accidents

Progressive, The General, Bristol West

That’s all for today folks! Hope your Monday is great and your coffee is strong!

Any questions? I “Noah” guy. Comment below or reach out to me via email: Noah@Theelinsurance.com

I don’t know who needs to hear this, but pushy sales tactics and “selling the dream” over the phone are exactly why so many agents and agencies fail.

Whether you’re cold calling or working warm leads, you’re doing your clients a disservice by trying to force your product with your preferred coverages down their throat.

Just listen to what they actually want. Offer your professional advice—that’s your job. But for the love of God, stop telling people they don’t know their own needs.

Even worse, too many folks in this industry are flat-out misleading. A prime example? Pushing the idea of “full coverage” without ever explaining liability limits or deductibles.

Sure, you can churn and burn a quick sale—but don’t expect to keep that business.

Renter’s Insurance doesn’t have to be a difficult concept to understand. Unfortunately, with so many people in my industry simply salivating over the idea of selling you another product, they tend to glaze over the purpose for renter’s insurance. I’m going to break this down in a way that simplifies it and helps you identify why you might need renter’s insurance for yourself. As always, TLDR at the bottom if you’re in a hurry.

When I talk to people about Renter’s Insurance, I tend to get three different reactions;

“What does it cover?”

“My landlord says I have to have it, so sure I’ll take it.”

“Why do I need it?”

Less commonly, I find people who think they’re protected by their landlord’s insurance policy. Unfortunately, this is a misconception that can cause catastrophic results in case something happens.

Renter’s Insurance Coverages

Renter’s Insurance is typically broken down into three different parts for which you are covered;

Personal Property

Liability Protection

Additional Living Expenses (ALE)

These three coverages work in tandem to keep your protected and prepared – and usually for less than $20 a month. Let’s break down the purpose of each coverage;

Personal Belongings: It covers your personal items—like clothing, electronics, and furniture—against risks such as theft, fire, vandalism, and certain types of water damage. Make sure to check if your policy offers replacement cost coverage (which reimburses you for the current market price to replace your items) or actual cash value (which accounts for depreciation).

Liability Protection: This section protects you in case you’re held responsible for injuries or property damage to someone else. For example, if someone is injured in your rental or you accidentally damage another person’s property, liability coverage can help cover legal and medical expenses.

Additional Living Expenses (ALE): If a covered event—like a fire—renders your rental uninhabitable, ALE covers the extra costs you might face for temporary housing, such as hotel stays or renting another apartment.

These components work together to give you financial protection when unexpected events occur. However, it’s essential to review the specifics of your policy, as coverage details and exclusions can vary between insurers and regions.

TLDR:

Renter’s insurance protects your personal belongings against losses like theft and fire, provides liability coverage if you’re responsible for injuries or property damage, and covers extra living expenses if your rental becomes uninhabitable due to a covered event.

Additional questions? Email me at Noah@theelinsurance.com or comment below!

I remember when I got my first car at 19 – a 1985 Toyota Tercel. When it was time to buy my first insurance policy, it was just as confusing as you’d expect. Insurance agents and brokers often use so much jargon that it makes things even harder to understand. My goal is to break down these complicated concepts so they’re easy to understand—like explaining it to my 4th-grade students! TLDR at the bottom if you don’t have time for in-depth reading.

When you’re buying car insurance, there are four main types of coverage (at least in Kansas) that you’ll usually discuss with your agent or insurance salesperson. By the end of this, you’ll be more informed about what to look for when shopping for car insurance.

Which coverages are required in Kansas?

Kansas, like many states, only requires four basic types of coverage: Liability, Medical Payments, UM (Uninsured Motorist), and UIM (Underinsured Motorist). Along with these, you’ll have coverage limits that apply in case of an accident. Let’s start with Liability.

Liability Coverage Liability covers damages or injuries to others when you’re at fault. If you cause an accident, you are “liable” for the damage. For example, if you rear-end someone while texting, or crash into a parked car, your Liability coverage will pay for the damage, up to your coverage limits.

There are two types of Liability coverage:

Bodily Injury Liability – This covers medical costs if you hurt someone in an accident.

Property Damage Liability – This covers the cost of repairing or replacing someone’s property (like their car, mailbox, or fence) if you damage it in an accident.

Below is a table of some common liability limits, as well as a brief explanation. If you have more questions about limits, don’t hesitate to ask in the comments below.

Bodily Injury

Property Damage

$25k per person/$50k per occurrence

$25k per occurrence

$50k per person/$100k per occurrence

$50k per occurrence

$100k per person/$300k per occurrence

$100k per occurrence

These limits are paid at a “per occurrence,” basis, which means for every accident you get into, you’re subject to that limit. In short, your limit won’t become less because you’ve had an accident. Your limit remains the same no matter how many accidents you have, unless of course, you and your agent change the terms of your policy.

UM/UIM Coverage (Uninsured/Underinsured Motorist) This coverage protects you if the other driver doesn’t have insurance or doesn’t have enough insurance to cover the damage they caused. It also helps if the at-fault driver leaves the scene (a hit-and-run). Like Liability coverage, UM/UIM coverage has limits that apply per accident. See the table below for some common UM/UIM limits.

Common UM/UIM coverage limits

$25k per person/$50k per occurrence

$50k per person/$100k per occurrence

$100k per person/$300k per occurrence

Just like your liability, UM/UIM claims are paid out per occurrence, and one claim will not diminish your limits for the next. If you’ve got questions about these limits, feel free to ask in the comment section!

Medical Payments Coverage

Of all of these required coverages, Medical Payments Coverage is the simplest. Without going too deep into it, simply put, Medical Payments Coverage helps to cover medical expenses for you and your passengers no matter who was at fault. Much like the other coverages discussed here, this is subject to the limits outlined in your policy.

What Does Full Coverage Come With?

“Full coverage” is a term that can be confusing. It doesn’t mean you’re fully covered for everything—it just means you have Liability, UM/UIM, Medical Payments, and two additional coverages: Comprehensive and Collision. These two coverages protect your vehicle and come with a deductible. The deductible is the amount you pay out of pocket before your insurance covers the rest of the repair costs.

Comprehensive Coverage: This covers your car if it’s damaged by something outside of your control, like a tornado, hailstorm, or a deer jumping in front of your car while you’re driving.

Collision Coverage: This covers your car if you crash into another vehicle or an object, like a tree or fence.

What is a Deductible? Your deductible is the amount you have to pay when you file a claim for damage to your car. For example, if your deductible is $1,000, you’ll pay the first $1,000 of repair costs, and your insurance will cover the rest. If you choose a higher deductible, your monthly premium (the amount you pay for insurance) might be lower. But, be careful not to choose a deductible too high—make sure it’s an amount you can afford to pay if something happens.

TLDR:

In Kansas, car insurance requires Liability, Medical Payments, UM/UIM coverage, and Personal Injury Protection. “Full coverage” adds Comprehensive and Collision coverage, which protect your car from damage. These coverages come with a deductible, which is the amount you pay before insurance helps with the repair costs.

Additional questions? Email me at Noah@theelinsurance.com or comment below!